How can we build a truly resilient Canadian wool sector?

Okay everybody. Better strap in! We’re getting into it.

Wool is one of those quiet agricultural products that most people rarely think about — until, suddenly, there’s a sweater on their back, insulation in their walls, or a blanket on their bed.

Canada has a long – long! – history of sheep farming and wool production, but in recent decades the nation’s wool industry has struggled to maintain the infrastructure needed to capture real value from its clip (a clip is just the total amount of fleece shorn from sheep across Canada – approximately 3 million pounds annually). In 2023, the average price paid to Canadian wool producers was just $0.35/kg ($0.16/lb) and the total volume of raw wool purchased directly from farms declined roughly 48 per cent from the previous year – a sign of shrinking market channels and weak returns for producers leading to an overall decline in attention and investment in wool, the start of a vicious circle. With less money to be made in wool sales, farmers didn’t make the same effort to keep fleeces clean, improve wool genetics in their flocks or store sheared fleeces appropriately. This in turn led to a further reduction in expertise over time – fewer people skirting and sorting fleeces and less standardization when it came to assessing and grading fleeces for future use.

Historically, the Canadian Co-operative Wool Growers (CCWG or just “wool growers” in farmer short-hand) played a central role in collecting, grading and marketing much of the national clip. Today however, CCWG’s involvement in purchasing wool has been minimal, returns are low and much of their stored wool inventory has been sent abroad to be processed into pellets, the lowest potential value. At the same time, advocacy and industry-focused groups like the Canadian Wool Collective, the Canadian Wool Council and Campaign for Wool Canada are working to re-energize the sector but these organizations do not function as commercial market intermediaries – they’re not buyers. These groups of passionate and dedicated folks from across the sector are doing their best to build demand but they can’t provide an alternate avenue for wool sales. They may be able to drum up public and even industrial support, but they don’t put Canadian wool on shelves or into an assembly line – some of the links are missing.

To rebuild a value chain that works – that pays meaningful returns to conscientious producers and a trusted and consistent supply to potential industrial-sized buyers – we need to break it down into three chunks, each of which has to be fully functional, integrated with each other and filled with good-quality Canadian content. Imagine the entire supply chain as your grocery cart. Inside the cart you have three bags and inside each bag are the essentials for one great meal. The cart is the Canadian supply chain, the bags and their contents (the raw materials) are the processes and product needed to get to the main, for-the-public event, a delicious and balanced end result that does exactly what’s promised.

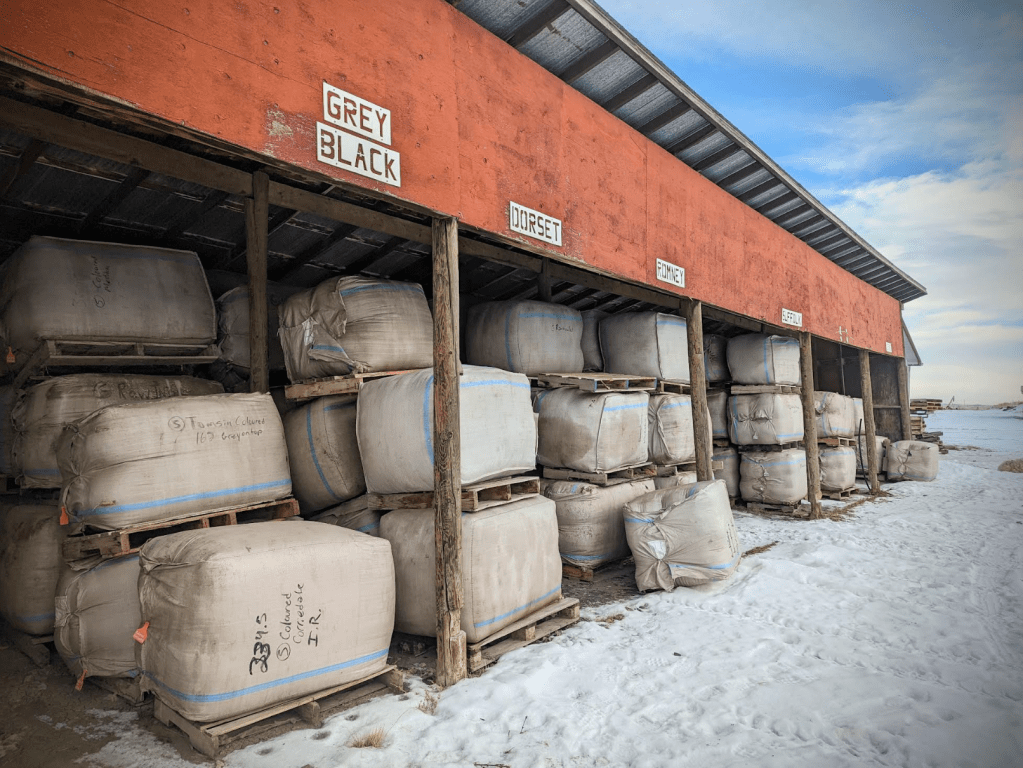

Quality Filtering – Standardized Wool Classing and Preparation

Raw wool varies widely in fibre diameter (micron count), staple length, cleanliness and breed characteristics. My own Border Leicester fleeces (here’s an example of one fleece analysis in my flock to give you an idea) generally have a coarser micron count – somewhere in the 22-26 micron range with a staple length after one year of anywhere from eight to 10 inches but both of these measurements can change depending on the individual. Other breeds, like Dorsets or Southdowns, will have a shorter fleece length – maybe three to four inches – and a finer micron, again with some individual variation. While these don’t necessarily seem like huge differences, in an industrial process, variation is verboten. Manufacturers are looking for repeatable consistency within a narrow range. And since most Canadian sheep are bred for meat and fleece is an after thought, many of our commercial animals are mixed breeds. Crossbred animals can vary enormously in their fleece characteristics and with something like 52 different sheep breeds in Canada, the potential for a wide range of fleece types is enormous once crossed genetics come into the picture.

While manufacturers rely on volume and consistent, predictable quality definitions, what we have in Canada is a growing divergence away from the basic building blocks. Wool classing is the work that stands between these buyers who need to know exactly what they’re buying and the producers who grow the fleece. Classing – sometimes used interchangeably with grading even though they are not the same thing (such is our loss of expertise in Canada that even the definitions for these wool handling basics gets muddled) – is a hands-on process that gives buyers that assurance by sorting fleeces into specific grades using a range of different observed and measured criteria.

Most of that knowledge was concentrated in CCWG and as they have increasingly stepped away from this work, there’s now a gap in the system – without standardized classing, potential buyers are understandably hesitant to engage. And for producers, a lack of real return – commodity-level pricing that treats every fleece the same regardless of its actual condition – disincentivizes time investment. When producers stop seeing a benefit to keeping wool as clean as possible, they don’t. When wool is contaminated, buyers (wherever they are) don’t step into the value chain. With fewer buyers, there’s less buy-in from producers . . . and the cycle continues.

There’s an opportunity here – a national classing standard and certified classer training program would stand where producers and buyers meet, the check-out of our metaphorical grocery cart. This quality foundation is essential for everything that comes afterward. It strengthens buyer confidence that Canadian wool will consistently meet specifications, perform to standard, work in their processes and produce a reliably desirable product those manufacturers can sell down the value chain. It also allows producers the discrimination to ear-mark certain fleece lots for certain buyers – some fleeces may go to custom processing or for the artisan market where returns are highest but volumes are small, some may go to manufacturing customers where returns are moderate but volumes are high. A classing standard allows wool to be appropriately streamed to its best fit-for-purpose outcome and in so doing, it reduces (and hopefully eliminates) waste in the system. No more mouldering wool piles gently composting in out of the corners of the barn.

Aggregation and Logistics: Building Market-Sized Lots and Preserving Quality

Most commercial wool buyers – textile mills, insulation manufacturers and other large-volume customers – don’t purchase raw, greasy wool one bag at a time. They typically require large quantities of cleaned (the term we use is “scoured”) wool, often in hundreds-of-thousands of pounds.

For example, a factory in Ontario – the country’s manufacturing heartland (and the part of the province I come from) – might want to buy 250,000 pounds of scoured wool. To produce that much scoured wool, a scouring plant would need to take in almost double that weight of raw wool – 500,000 pounds – since most wool loses somewhere close to half its weight when it’s scoured. Turns out all that lanolin, dirt, vegetable matter and suint is surprisingly heavy. Down-style breeds (like Southdowns, Suffolks and others) tend on the whole to be greasier than longwool-style – sometimes called strong wool – breeds, like Lincolns, Teeswaters and Border Leicesters.

Before any of it can be scoured, it has to be:

- Skirted (removing any contaminants which can range from organic matter like poop, seeds, sticks, chaff, hay to plastics or anything else that shouldn’t oughtta be there)

- Sorted and classed into uniform, quality categories

- Stored in conditions that maintain quality (humidity and temperature control, no bugs, no varmints)

- Aggregated or gathered into large lots that can accommodate the scale an industrial customer requires

In Canada currently, we don’t have any large-scale scouring capacity. Nada. If industrial-scale scouring is required, we must look beyond our borders to the United States where only a handful of commercial scourers currently operate – Chargeurs in South Carolina and Bollman Industries in Texas are the two that come to mind.

Small-lot scouring options do exist across the country at so-called “mini mills” (these are often, though not always, Belfast mini mills, made in Nova Scotia). Unfortunately, these mills can’t replace the bulk capacity needed to serve large buyers. Without regional gathering hubs – this is exactly the kind of thing CCWG used to do – processors often leave wool in storage for extended periods while they accumulate necessary volume. The storage element adds cost, increases risk of something gross happening (moths! mouses!!) and brings in a staggering level of logistical complexity – borders to cross, trucking to arrange, customs/duties, the nefarious dealings of capricious authorities. . . You get the idea.

The opportunity here is investing in regional depots – just like the ones CCWG operated – where classed wool is collected, properly stored and prepared for large-scale processing AND (because both would future-proof a resilient supply chain) building scouring capacity domestically.

Finding Buyers: Sales, Contracts and some Pricing Truth

Oof. This is the “ugh” element. Stick with me now.

Once wool is classed and gathered into large lots, it still needs to find buyers. There is a need for commercial relationships, contracts, pricing transparency and sales channels that connect supply and demand. In other countries, this is often done at an auction – lots of wool come up sorted into appropriate grading categories and marked by weight. Wool buyers representing specific customers purchase required amounts, arrange the next-step logistics and then the wool is sent all over the world. That’s the current model.

In Canada however, there is not currently a functional national marketing entity (note, I said “functional”) and many producers rely on ad-hoc buyers or export markets, often getting low returns relative to the potential quality of their clip. Investors, brands and buyers all benefit when supply comes with clear documentation of quality, origin, quantity and logistics – providing that kind of paper trail requires organization and currently, we don’t have it.

Having said all that, it’s important to point out that the way they may do wool in New Zealand or Australia doesn’t necessarily need to be imported to Canada. Both those countries have much, much higher sheep populations and are much, much smaller than Canada. Given our unique geography and the characteristics of our flocks, a made-in-Canada bespoke wool solution might be a better option. If it builds domestic capacity and a resilient and reliable supply chain, the goal will have been met, however we got there. This part of the equation invites innovation, creativity and flexibility, qualities Canadians have in spades by virtue of necessity. What we need is someone to apply some Canuck-style chutzpah and come up with a solution. Have at ‘er, I say.

A Roadmap For Investors and Innovators

To turn Canada’s wool industry into a viable economic engine for all Canadians, we need a multi-stage strategy. There has been a ton of chatter on this front for some time – Campaign for Wool Canada set out a “Wool Plan” (this document is currently under review with a new five-year plan due in early 2026) and other groups are bending their very-busy-brains to just this effort. As I see it, here’s the birds-eye-view:

- Step 1 – (Re)build the Foundation: Quality Infrastructure

Establish and scale a national classing standard with certified classers; provide training and tools so producers can prepare fleeces that meet buyer specifications and expectations. This would reduce risk for buyers, improve product consistency and lift quality premiums incentivizing producers to grow fleeces to the highest standards - Step 2 – Regional Collection and Aggregation

Create some kind of regional collection process where classed fleece is stored, monitored, prepared and designated into market-ready lots. Potentially partnerships, co-ops or other Canadian-centric models might be explored. Long-term storage (risk and cost) could be mitigated while also improving scale for future processing, essential building blocks for wool in Canada. - Step 3 – Processing Connectivity

Invest in Canadian scouring capacity at a scale that works for Canadian industrial buyers. Failing that, negotiating long-term capacity agreements with existing scouring facilities abroad. Perhaps there are value-added partnerships that can absorb graded volumes domestically, perhaps there are creative and unexpected relationships that can be expanded. If these gaps and opportunities could be fully leveraged, it could capture more value in Canada (raw, mid and finished processing in Canada benefitting Canadian companies, Canadian communities, Canadian workers and Canadian consumers) reinvigorating rural communities and mitigating freight costs across our vast geography. - Step 4 – Market Commercialization

Pricing and origin transparency are essential to really capitalize on the future of Canadian wool. Integrating the awesome storytelling already being done by Campaign for Wool Canada and the Canadian Wool Collective among others helps Canadian buyers, sellers, processors and customers to reframe value. Emphasizing Canadian innovation and creativity and backing it up with verifiable data regarding sustainability and traceability builds confidence, draws long-term contracts and improves producer returns. Encouraging producer participation in standardization and certification and labeling – like “Made in Canada” or “Certified Animal Welfare Approved” or “Regenerative” – builds higher levels of potential return for producers while also allowing premium mark-ups for processors/manufacturers and retailers.

The Path Forward

There is real value in Canadian wool. Many of us don’t need to be convinced – we’re already fully on board. However, without functional quality standards, infrastructure and a professional arena to bring all the players together, we are on the back foot, scrambling to keep up like sheep on ice. In the current state of affairs, we are allowing value to leak away from every layer and player in the value chain.

With targeted and strategic investment, innovators and investors could transform the industry from a balkanized and fragmented landscape – producers here, processors here, manufacturers here, customers here – into a coordinated, resilient supply chain that captures and holds value for fibre grown on Canadian farms. Period.

All the opinions expressed in this column are my own, gathered after years of simply talking to producers and players at every point in the value chain. I don’t consider myself an expert – my Dad says ‘X’ is an unknown quantity and “spurt” is just a drip under pressure – but I do consider myself informed. For more on Canadian wool and material culture, check out our Material Culture resource page under Keeping in the Navigation bar.

This is a Living post, a post to share my thought processes, where my priorities lie and the philosophy that underpins our activities here at the homestead. It is not a how-to, “expert advice” or meant to reflect a wider experience than just my own, on my farm, here with my sheep.

Leave a comment